Innovative AndroidTV™, Linux, and RDK-powered video solutions and smart media devices enable you to deliver high-quality video services with a modern, AI-enhanced user experience including live TV, streaming, advanced surround-sound, and beyond.

From high-definition satellite, off-air, and streaming headend solutions to revolutionary 4K UHD video management systems, Vantiva’s multi-client solutions offer everything you need to elevate the customer experience while satisfying content owners.

Today’s consumers have choices. They demand better, faster, more reliable, and affordable services. Earning satisfaction and loyalty means providing the best customer experience possible — and our extensive experience and expertise in the connected home will ensure you do just that.

ECO Service Management is a cloud-based platform that simplifies the delivery of next-generation services and manages the complexities of blending emerging consumer devices and next-generation technology. It supports mission-critical service management that empowers customer support, operations, and subscribers.

Technicolor: Full Year 2021 Results and planned listing of Technicolor Creative Studios

Paris (France), February 24th, 2022 – Technicolor (Euronext Paris: TCH; OTCQX: TCLRY) is today announcing its results for the full year 2021. The Board of Directors of Technicolor SA, meeting on February 24th 2022, approved the Group’s full year 2021 accounts.

Technicolor met its 2021 guidance, despite numerous headwinds

2022 looks strong and Technicolor confirms its 2022 guidance

Technicolor intends to list Technicolor Creative Studios (TCS) to enable its further growth and development in line with strong industry demand:

Technicolor intends to list and spin-off 65% of Technicolor Creative Studios through a distribution-in-kind to Technicolor shareholders, while Technicolor will remain listed on Euronext Paris and post-Spin Off will retain up to 35% ownership of TCS

Evolution into two industry-leading, independent listed companies, each with the ability to pursue its own strategic agenda and unleash value potential

Technicolor intends to further deleverage so that both companies can have more active development profiles, through a refinancing of the entire existing debt structure, and the issue of €300m of Mandatory Convertible Notes (“MCN”) whose conversion into Technicolor shares would be effective upon the execution of the spin-off. This MCN is a key component of the spin-off process and is supported by selected subscribers who have committed to subscribe to the full amount

Technicolor has received a binding offer to sell its Trademark Licensing operations for c.€100 million in cash, subject to closing conditions, with completion expected in H1 2022. This is another step in the direction of further deleveraging and simplification

Richard Moat, Chief Executive Officer of Technicolor, statement:“2021 was a year of great success despite the volatile business environment, and we have yet again proved our ability to react quickly and efficiently to unexpected challenges. The efforts of our dedicated teams have enabled us to achieve our 2021 guidance, and I want to thank everyone around the world who contributed to this excellent result. The outlook is strong, and today I am pleased to confirm our 2022 guidance. The transformation of the Group carried out over the past two years has resulted in us having three profitable businesses which are global leaders in their respective markets. In addition to executing our transformation program, the Board of Directors and management team have continuously evaluated strategic options to unleash the value potential of our divisions. After a comprehensive review, we determined that pursuing the partial spin-off of TCS from the Group along with the full refinancing of the existing debt will be the solution that best aligns strategy, value creation and financial objectives for all of Technicolor’s stakeholders. We are convinced that this operation is a unique opportunity to ensure both TCS and Technicolor Ex-TCS have the adequate capital structure to support their developments, long-term ambitions and organic growth. The execution of these operations will allow both companies to pursue their own strategic agendas, be more agile and ultimately thrive as independent businesses.”

2021 Key Highlights & 2022 Outlook

Technicolor met its 2021 guidance for the full year, with adjusted EBITDA reaching €268 million, adjusted EBITA €95 million and Free Cash Flow before Tax and Financial €(2) million. Revenues declined by 1.7% at constant exchange rate. Technicolor Creative Studios recorded a strong improvement in revenues, while Connected Home was impacted by industry-wide key component shortages and supply chain disruption which prevented the business from meeting strong customer demand in full. Adjusted EBITDA improved by €109 million at constant exchange rate, representing a 9.3% margin, up 379 basis points, as a result of the significant cost savings and operating efficiencies achieved across all divisions. Similarly, adjusted EBITA increased by €155 million at constant exchange rate. Operational improvement was also reflected in the €119 million Free Cash Flow improvement at constant rate, resulting in €(2)m Free Cash Flow (before financial results and tax) from continuing operations. Net debt IFRS amounted to €1,039 million as of December 31, 2021 compared to €812 million at the end of December 2020, leading to a Net Debt / EBITDA ratio of 3.87x at constant exchange rate, in line with guidance.

Outlook

The Group confirms its 2022 guidance:

Demand for Technicolor Creative Studios’ highest quality VFX artistry and cutting-edge technology is expected to continue to grow significantly throughout 2022. The division has been awarded multiple new projects, resulting in approximately two thirds of the revenue pipeline for MPC and Mikros Animation being already committed for 2022. Significant investment in artist recruitment, retention and training (including TCS Academy programs) will continue.

Worldwide demand for Connected Home broadband equipment is expected to remain strong in 2022. Ongoing component shortages and pricing challenges will continue to restrict our ability to serve end customer demand; nonetheless, efficiency measures, progressive improvements in delivery and continuous discussions with both suppliers and customers should help compensate for these negative factors.

In DVD services, improving format mix driven by higher year-on-year new release volumes as theatrical attendance continues to normalize, along with further cost efficiencies, are expected to mitigate the anticipated modest disc volume decline. The division is working on further significant expansion of non-disc activities.

The Group delivered €171 million of cost savings in 2020, and €116 million in 2021. These results, combined with continuous improvements in efficiency, are keeping Technicolor on track to deliver a cumulative €325 million in run rate cost savings by the end of 2022. As a result, the Group Technicolor confirms its 2022 guidance:

Revenues from continuing operations are expected to grow,

Adjusted EBITDA from continuing operations of €375 million,

Adjusted EBITA from continuing operations of €175 million,

FCF from continuing operations, before financial results and tax of €230 million.

2022 guidance was confirmed on November 3, 2021, assuming constant €/$ exchange rate of 1.15. 2022 guidance numbers presented in this press release have been restated to reflect changes in accounting methods (IFRIC adjustments on Saas). More details on adjustments are available in the Additional Financial Information paragraph in section II.

Intention to list Technicolor Creative Studios to enable its further growth and development, creating two independent market leaders, and to refinance Technicolor’s existing debt

Rationale of the contemplated transactions

Over the past 2 years, Technicolor’s management has transformed the Group by restructuring operations and restoring profitability, despite the challenges brought by COVID-19. Today Technicolor operates three profitable businesses, each a leader in its respective market. As the operational and financial transformation of our businesses progressed, our Board of Directors and management team have continuously reviewed strategies to unlock value to all of Technicolor’s stakeholders. Today’s announcement on the proposed spin-off of a 65% stake in TCS, and the intention to refinance our existing debt, allows the Group to set out on a path towards unleashing the full potential of our businesses. It also marks, along with the Mandatory Convertible Notes, a further and significant expected deleveraging of both new entities, notably for TCS on a stand-alone basis which is expected to benefit from a leverage in line with market peers. Within the framework described above, Technicolor’s Board of Directors has approved the plan to list and partially spin off TCS. The current perimeter of Technicolor activities would therefore be divided into:

Technicolor Creative Studios (“TCS”);

Technicolor Ex-TCS, which will comprise Connected Home and DVD Services, and is expected to retain up to a 35% stake in TCS at the time of the spin-off.

TCS and Technicolor Ex-TCS have distinct characteristics in terms of growth, margins, capital intensity, and cash flow generation. The contemplated transaction will allow each entity to pursue its own strategic path independently, consistent with its underlying business dynamics and financial fundamentals, and thereby achieve its full value potential. Furthermore, the spin-off of TCS should help to reduce the conglomerate discount of Technicolor Ex‑TCS and create a strong basis for TCS full valuation. TCS is a global leader in VFX, offering a unique ‘pure play’ equity story in a market experiencing exponential growth driven by burgeoning demand for content. TCS will have a Board of Directors and a management team independent from Technicolor Ex-TCS. As a separate company with direct access to capital markets, TCS will be able to accelerate the execution of its strategic agenda and growth trajectory. Technicolor Ex-TCS will strengthen market leader status in Connected Home and DVD Services. The company is expected to have a stronger balance sheet following the contemplated refinancing, with lower leverage and greater liquidity than today, hence significantly de-risking its financial profile. Connected Home and DVD Services will therefore be in a strong financial position to reinforce their status as global players.

Contemplated spin-off details

Technicolor intends to list TCS on Euronext Paris, and to make a concurrent distribution of a 65% stake in TCS to Technicolor shareholders (the “Distribution”). The spin-off structure allows Technicolor shareholders to receive Technicolor Creative Studios shares, while remaining shareholders of Technicolor Ex-TCS. In view of the analysis to date of the composition of Technicolor SA’s net equity and in particular its negative retained earnings which the projected 2022 income (including the capital gain on the transfer of the TCS shares) is not expected to absorb, it is to-date anticipated that this distribution-in-kind would be made out of Technicolor’s share premium account, and that it should, from a French tax perspective, be considered as a tax-free return of share premium under article 112 of the French tax code (remboursement de prime d’émission). This Distribution should therefore not be subject to tax in France whether by way of a French levy, a French withholding tax or otherwise (subject to specific situations). Additional information will be provided in this respect ahead of the actual distribution. As far as the remaining 35% TCS stake retained by Technicolor Ex-TCS is concerned, its disposal will be considered ahead of or following the spin-off, depending on market conditions, with a view to further and significantly deleverage both new entities. The spin-off resolutions will be submitted to the Company’s Annual and Extraordinary Shareholders Meeting that it is anticipated will be convened in late June 2022. It is expected that the spin-off will take place during the later part of Q3, 2022 subject to the conditions outlined below. The company will request the admission of the TCS shares on Euronext Paris by way of a prospectus to be approved by the AMF. The company has retained Finexsi as independent financial appraiser in order to provide shareholders with an independent valuation of the TCS shares prior to the vote at the Company annual shareholders’ meeting referred to above.

Contemplated refinancing package details

Concurrently, Technicolor is announcing its intention to fully refinance the Group’s debt. As part of the refinancing, Technicolor intends to issue Mandatory Convertible Notes (“MCN”) for €300 million in the form of separate reserved issuances. Angelo Gordon, Bpifrance and other selected subscribers have committed to subscribe to the full amount of the MCN. The MCN would automatically be converted into Technicolor shares if a Technicolor Extraordinary General Meeting approves the Distribution, and the Board of Directors decides such Distribution. The conversion price of €2.60 per share is equal to a 5% discount to the 3-month VWAP (“Volume-Weighted Average Price”) per Technicolor ordinary share as of February 23rd, 2022. The fairness of the condition of the Mandatory Convertible Notes conversion will be addressed prior to the vote at the MCN Extraordinary General Meeting by a report to be prepared by Finexsi as independent financial appraiser. The issuance of the MCN is subject to 2/3rd majority approval at an Extraordinary General Meeting of shareholders, which is expected to take place early Q2 and, in any case, no later than May 25th, 2022. Shareholders subscribing to the MCN have committed to not dispose of their shares before the MCN Extraordinary General Meeting. In parallel, consistent with the proposed transaction, the Group is launching negotiations to refinance its existing debt, with a view to putting in place two distinct and optimized financing packages for TCS and Technicolor Ex‑TCS respectively.

The refinancing and the spin-off are expected to be completed by Q3 2022, subject to (i) the shareholders’ approval of the issuance of the MCN, (ii) the shareholders’ approval of the terms of the spin-off, (iii) the completion of the refinancing discussions with creditors on terms satisfactory to Technicolor Ex-TCS and TCS and (iv) customary conditions, consultations and regulatory approvals.

Technicolor Creative Studios: a collaborative global VFX leader driving innovation and creativity

TCS provides its clients with the highest quality VFX artistry and cutting-edge technology in the industry. Following the appointment of Christian Roberton as President in 2020, TCS has been fully reorganized to run in a more efficient and agile way. The studios have been integrated under dedicated business lines with MPC for Film & Episodic VFX, The Mill for Advertising, Mikros for Animation and Technicolor Games to serve the gaming industry, achieving significant synergies and efficiencies. Each of the business line is supported by fast growing markets, together with a unique opportunity to play a central role in new areas such as the creation of the metaverse. In addition, the newly listed company will benefit from unique technological expertise, longstanding customer relationships, a large-scale production platform in India, a unified pipeline toolset, and access to unique talent pools supported by its world-leading Academy training programs. With the proposed spin-off, TCS is making a further step to accelerate organic growth and expand into scalable markets, capitalizing on the wave of burgeoning demand for content. Its ambition is to reinforce its status as the leading collaborative global VFX player, driving innovation and creativity through growing and evolving environments for filmmakers, brands, games companies, streamers and the metaverse. Technicolor Creative Studios is led by an experienced, proven management team, and industry-leading creative talent and technologists. Christian Roberton will be appointed CEO of the new entity, and Anne Bouverot will be proposed as Chairperson of the Board of Directors. As an independent company, TCS will have greater agility and flexibility to achieve its financial targets. It will be well-positioned for EBITDA expansion and strong cash flow generation, enabling it to become a consolidator in its markets, unlocking value for its current and future stakeholders. TCS will be headquartered in Paris, France and will apply for listing on the regulated market of Euronext in Paris.

Technicolor Ex-TCS: a leader in its segments with a stronger balance sheet

Technicolor Ex-TCS core activities will be composed of two businesses having leading positions in their respective markets and with solid fundamentals ahead:

Connected Home is the leaderin Broadband and Android TV.

DVD Services is the worldwide leader in replication, packaging and supply chain solutions for packaged media and related products, serving global content producers across film, television, games, and music.

The Group will benefit from a stronger balance sheet, and greater liquidity, significantly de-risking its financial profile and providing the foundations for value creation potential. Over the past 2 years, our renewed and experienced management team has driven the transformation of the Group. We have improved the resiliency of the business models of both Connected Home and DVD Services and proved our ability to react fast and to adapt efficiently in facing headwinds such as supply shortage. At Connected Home, under the leadership of Luis Martinez Amago, we adopted a platform-based approach, optimizing our product lines, and refocusing our customer portfolio, as well as streamlining our operations through supplier selectivity and cost reduction. This has enabled Connected Home to successfully reposition itself towards two growing markets: high end broadband gateway products and diversification into Android TV in the set-top-box segment, leveraging best-in-class supply chain and integrated R&D capabilities to reduce time-to-market. DVD Services has evolved into a Specialist Manufacturing & Supply Chain Services division under David Holliday, President since 2020. To accomplish this, he and his team have been working since the start of 2020 on a complete business transformation of the division, which has involved the closure of 13 facilities and relocation of several operations along with cost reduction and efficiency measures. It has repositioned its disc activity into a profitable volume-based business. In parallel, the division has rapidly evolved its vision and established four new growth businesses which leverage existing assets, proven capabilities and expertise. Diversification is now being accelerated, through manufacturing services, including vinyl and biodevices, and supply chain and fulfillment services and solutions. These new growth businesses are expected to provide a positive contribution to the division’s revenues and profitability in FY22, with significant growth anticipated for the following years. Post separation, Luis Martinez Amago will be appointed CEO of Technicolor Ex-TCS, and Richard Moat will be proposed as Chairman of the Board of Directors. This process is a unique opportunity which will provide Technicolor Ex-TCS with additional financial headroom for growth, diversification and competitive positioning. The combination of spin-off and refinancing will significantly reduce the risk-profile of Technicolor Ex-TCS, providing it with a deleveraged balance-sheet and increased liquidity. Technicolor Ex-TCS will remain listed on the regulated market of Euronext in Paris, with headquarters in Paris.

Advisors

Goldman Sachs, Morgan Stanley, Rothschild & Co. and d’Angelin & Co. are acting as financial advisors to Technicolor. Bredin Prat and Kirkland & Ellis are acting as legal advisors to Technicolor. Gide Loyrette Nouel is acting as legal advisor to Technicolor Board of Directors.

Sale of Trademark Licensing operations

Technicolor received a binding offer to sell its Trademark Licensing operations. The total agreed consideration amounts to approximately €100 million, to be paid in cash at the closing of the transaction.

This transaction allows the Group to further simplify its structure with the sale of non-core assets, and to increase Technicolor financial flexibility.

The sale, which is subject to closing conditions, is expected to close in the first half of 2022.

Additional Financial Information

In the period preceding today’s announcement, as part of the process, the Company shared forward looking assumptions with some of its shareholders who will participate in and/or support the transactions. These assumptions, elaborated at the end of Q3 2021 and based on market conditions assumptions prevailing at the time, are currently under review by the Group.

Forward looking assumptions provided for Technicolor:

For 2024, a key assumption for Technicolor was the acceleration of growth driven by continuous operational and end-market improvements. In addition, as part of the process, the company shared, with some of its shareholders who will participate in and/or support the transactions, further forward looking assumptions for TCS and Technicolor Ex-TCS.

Forward looking assumptions provided for TCS and Technicolor Ex-TCS:

For 2024, key assumptions for TCS and Technicolor Ex-TCS were:

TCS: strong growth as a result of anticipated continued burgeoning demand;

Technicolor Ex-TCS: continued delivery of solid financial results driven by broadband and diversification in both CH and DVD Services activities.

In no case should 2023 and 2024 numbers be considered as future guidance. Guidance for TCS and Technicolor Ex-TCS will be established and disclosed at the time of the Capital Market Days that will take place at the end of May/early June. Data presented above:

Have been established using a 1.15 €/$ exchange rate;

Do not reflect the upcoming disposal of Trademark Licensing assets;

Include estimated running dissynergy costs of €30-40 million;

Exclude c.€ 75 million costs and fees associated with the transactions. These costs and fees include €30-40 million estimated refinancing costs including make-whole of the current debt, €25-30 million fees related to the separation, spin-off and distribution of 65% of TCS shares, and €10 million of other costs associated with both transactions;

Do not reflect the accounting changes implied by the IFRIC interpretation on Saas adjustments, relating to the configuration or customization costs in a cloud computing arrangement. The one-off impacts of IFRIC interpretation are expected to be material for 2022 as software capex were budgeted, resulting in a negative impact on EBITDA, a positive impact on capex and a neutral impact on cash. For 2022, they are estimated as follows:

Technicolor “as-is”: €(9) million on EBITDA, €(6) million on EBITA, +€9 million on capex

TCS: €(4) million on EBITDA, €(3) million on EBITA, +€4 million on capex

Technicolor Ex-TCS: €(5) million on EBITDA, €(3) million on EBITA, +€5 million on capex

For 2023, these impacts are expected to be less material.

In addition, the company will file a prospectus to be approved by the AMF as part of the TCS share admission process on Euronext Paris. TCS and Technicolor Ex-TCS intend to organize two Capital Markets Days at the end of May/early June, where updated guidance will be provided.

Governance

Katherine Hays has been appointed by today’s Board Meeting as a new independent Director in replacement of Cécile Frot-Coutaz who resigned as of September 1st, 2021. The decision being made by co-optation, it will be submitted to the ratification of Technicolor Annual Shareholders Meeting that will take place end of June 2022. Katherine Hays is an operational executive with more than 20 years of experience in the digital media and entertainment sector, notably as founder and CEO of the peer-to-peer marketing platform Vivoom Inc., CEO of visual effects software creator GenArt, and various management functions at Microsoft Startup Labs, MSN, Massic Inc, an in-game advertising platform she co-founded.

Segment Review – Full Year 2021 Results Highlights

Technicolor Creative Studios

echnicolor Creative Studios revenues amounted to €629 million in 2021, up 22.5% at constant rate year-on-year. Excluding the Post Production business divested in April 2021, year-on-year revenue growth at constant rate was 37.2%. This improvement, notably in the second half, resulted from significant demand for original content for all the business lines compared with 2020, which suffered from pandemic-related impacts on production in Hollywood and around the world. More precisely in 2021:

At MPC, revenues grew significantly driven by the continued ramp-up in production of major theatrical projects as well as increasing contributions from all the major streaming platforms;

At The Mill, advertising revenues grew across all key markets year-on-year, driven by a faster recovery in advertising spend from Covid than anticipated;

At both Mikros Animation and Technicolor Games, revenues grew significantly, driven by higher volumes across all segments.

The shortage of talent which impacted the entire industry was partly mitigated by significant retention and hiring action plans implemented during the year, with intense activity in the fourth quarter. During the year, TCS staff increased from approximately 7,700 at the end of December 2020 to approximately 10,560 at the end of December 2021. Adjusted EBITDA amounted to €113 million (17.9% margin), up €94 million year-on-year at constant rate, and Adjusted EBITA was €41 million, up €119 million year-on-year at constant rate. On top of the revenue increase, significant margin improvement resulted from the positive impacts of multiple operational transformation programs in conjunction with permanent cost reduction measures.

Connected Home

Connected Home revenues totaled €1,544 million in the full year 2021, down 10.0% at constant exchange rates compared with 2020. Sales volumeswere severely impacted by the worldwide semiconductor crisis combined with supply chain disruptions, limiting our ability to fully satisfy the strong demand from our customers. The underlying demand for 2021 was higher than our actual sales in 2020. Since the summer, the division has intensified its collaboration with clients and suppliers to maximize deliveries, and to mitigate potential profitability and working capital impacts, which paid off notably in the fourth quarter. The division continues to focus on selective investments in key customers, platform-based products and partnerships, and on optimizing fixed costs that will lead to improved margins over the year. Adjusted EBITDA amounted to €103 million in 2021, or 6.7% of revenue, flat at constant exchange rate. Margin was up 67 basis point as operating efficiencies and fixed cost savings offset lower volumes and the additional cost impact. 2021 Adjusted EBITA was €45 million, representing a 21.3% increase year-on-year at constant rate.

DVD Services

DVD Services revenues totaled €701 million in 2021, up 1.6% compared with 2020 at constant exchange rate. Despite slightly lower disc volumes year-on-year (-2.7%), revenue growth was driven by increased revenues from new growth businesses mainly in the US (distribution and freight revenues). Adjusted EBITDA amounted to €67 million, or 9.5% of revenues compared with 7.5% in 2020, up €15 million at constant exchange rate. Margin improvement mainly resulted from the significant year-on-year footprint optimization, further headcount reductions and higher activity in the North American non-disc activities. This upside was partially offset by the impacts of lower activity in the disc distribution business, higher labor costs in North America and Mexico, and higher raw material costs. DVD Services continued to adapt distribution and manufacturing operations, and related customer contract agreements, in response to continued volume reductions. Four significant facility closures (mainly in North America) were completed in 2021 as part of the ongoing transformation plan. Lower depreciation & amortization and renewal of contracts helped to deliver an Adjusted EBITA of €27 million compared to €(1) million in 2020.

Corporate & Other

Corporate & Other includes the Trademark Licensing business. Corporate & Other recorded revenues of €23 million in 2021 were in line with last year’s revenues of €23 million. Adjusted EBITDA amounted to €(14) million, and Adjusted EBITA was €(18) million.

Results Analysis

P&L Analysis

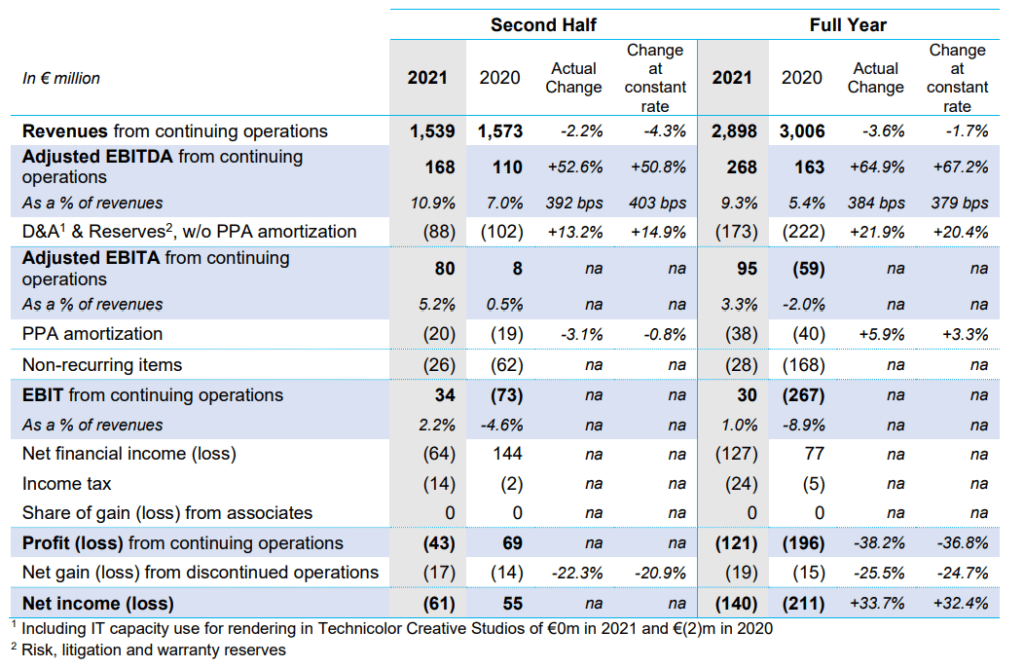

2021 Revenues stood at €2,898 million, representing a 1.7% decrease at constant exchange rate. The strong improvement of Technicolor Creative Studios, notably in the second half, was more than offset by lower revenues at Connected Home as a result of key component shortages and supply chain disruption which prevented the business from fully servicing strong customer demand. 2021 Adjusted EBITDA amounted to €268 million, up 64.9% year-on-year or 67.2% (or €109 million) at constant rate. The EBITDA margin increased by 379 basis points to reach 9.3% of revenues. This strong improvement reflects the rebound of Technicolor Creative Studios, along with costs savings and operational efficiencies at DVD Services and Connected Home. 2021 Adjusted EBITA of €95 million represented a €155 million year-on-year improvement at constant rate. This resulted from the EBITDA increase and the positive impact of efficiency measures, in particular lower D&A, following lower equipment spend and lower IP depreciation in Technicolor Creative Studios. This led the Group to overachieve its EBITA guidance of €60 million. Restructuring costs accounted for €(37) million at constant rate, including €(17) million in DVD Services, largely resulting from optimization of sites. Last year restructuring costs amounted to €(100) million. EBIT from continuing operations was a €30 million profit compared to €(267) million losses in 2020. This resulted from a better operational performance, while 2020 was impacted by DVD Services impairment and higher restructuring accruals. The financial result totaled €(127) million in 2021, compared to €77 million in 2020, reflecting:

Increased interest expenses of €(49) million, taking the total to €(126) million, primarily due to the higher interest rates on the new debt structure;

Other financial income was nil compared to €155 million in 2020, mostly explained by a non-cash gain on the equity and debt initial valuations in 2020 following the financial restructuring process.

Income tax amounted to €(24) million, compared to €(5) million in 2020. Net loss from discontinued operations amounted to €(19) million compared to €(15) million in 2020. Group net loss therefore amounted to €(140) million in 2021, compared to the €(211) million in 2020.

FCF and debt analysis

The strong improvement in FCF from €(124)m to €(2) million mainly reflects the improved operating performance at Technicolor Creative Studios. The change in working capital was €(81) million compared with €(103) million in 2020, which derived mainly from higher customers down payments and favorable payable variations at Technicolor Creative Studios resulting from higher activity in 2021. The key component shortage at Connected Home created an increase of unfinished goods inventory at Connected Home, notably in the third quarter, which was reduced through active cooperation with its clients and suppliers. While pension cash costs during the period were up by €4 million, pension liabilities were down by €(45) million mainly due to a positive effect from discount rates of €35 million, and payments of €26 million. Cash outflow for restructuring totaled €70 million in 2021, up by €24 million year-on-year at constant rate, mainly resulting from accelerated implementation of cost savings. Capital expenditures amounted to €95 million, down by €(6) million year-on-year at constant rate, as the Group maintained control over investment expense. The cash position at the end of December 2021 was €196 million, compared to €330 million at the end of December 2020. Cash generated by the operations was partly offset by cash outflows from interest payments and payments related to operating leases debt (IFRS 16). Net financial debt at nominal value amounted to €1,110 million at the end of December 2021, compared with €897 million at the end of December 2020, mainly due to change in cash and cash equivalent. IFRS net debt amounted to €1,039 million as of December 31, 2021, compared with €812 million at the end of December 2020, leading to a Net Debt / EBITDA ratio of 3.87x at constant exchange rate, in line with the guidance.

Covid-19 situation update

In 2021, Covid-19 affected immigration and travel, while creating logistics’ issues and shortages in certain components. The Group proactively addressed these issues to offset potential negative impacts and serve the growing demand for its operations.

At Technicolor Creative Studios:

Complying with evolving local and national government regulations, and in consultation with local business leadership, Technicolor Creative Studios continues to adjust capacity limits, on-premises protocols, and remote work policies.

In addition to immigration policy changes in Canada and in the UK, the pandemic continues to affect both immigration and travel, negatively impacting the industry’s ability to attract talent to locations where the demand for talent exceeds local supply. To support its significant backlog, Technicolor Creative Studios continues to invest in its Academies across multiple locations, and implements various measures aiming at reducing attrition rate and retain talents.

At Connected Home:

Connected Home remained operational due to the early adoption of a remote work model that successfully moved all non-engineering employees off site to ensure key engineering facilities remain safe and open.

In 2021 and 2022, Connected Home was impacted by both the direct effect of Covid (factories & R&D sites reduced productivity from time to time) and by the secondary effects: massive supply market disruptions, with all categories impacted, but integrated circuits & logistics by far the most. Supply & logistics disruptions are expected continue in 2022.

At DVD Services:

While theatrical new release activity remains partially suppressed, it continues to show an accelerating trend of improvement. Most major retailers continue to operate normally. Some production facilities continue to experience temporary staffing shortages, but the overall impact to operations remains manageable.

The ongoing Covid-19 impact will be dependent on the extent and duration of ongoing restrictions driven by the rate of new Covid case growth. DVD Services has accelerated certain aspects of its future restructuring plans in an effort to adapt to ongoing challenges, and has proven its resilience.

An analyst audio webcast hosted by Richard Moat, CEO and Laurent Carozzi, CFO was held on February 24, 2022, at 6:00pm CET.

Indicative timeline

Q1 2022 results MCN Extraordinary shareholders’ meeting Capital Markets Day for Technicolor Ex-TCS and TCS Technicolor’s AGM and EGM Spin-off of the TCS shares

May 5, 2022 No later than May 25, 2022 End of May / Early June 2022 End of June, 2022 End of Q3, 2022

Notes

2020 and 2021 break-down by region and products is available in Appendix 1 “Business hightlights by division” of this press release

(1) 2022 guidance numbers presented in this press release have been restated to reflect changes in accounting methods (IFRIC adjustments on Saas). More details on adjustments are available in the Additional Financial Information paragraph in section II. (2) Key terms of the MCN are presented in Appendix 7 (3) Source: September 2021 – Dell Oro (4) In addition to this amount, a break fee is also provided under the terms and conditions of the MCN in the event the MCN is not issued (5) Revenue break-down by region and products is available in Appendix 1 “Business highlights by division” of this press release. (6) Volume break-down by product is available in Appendix 1 “Business highlights by division” of this press release.

Warning: Forward Looking Statements This press release contains certain statements that constitute “forward-looking statements”, including but not limited to statements that are predictions of or indicate future events, trends, plans or objectives, based on certain assumptions or which do not directly relate to historical or current facts. Such forward-looking statements are based on management’s current expectations and beliefs and are subject to a number of risks and uncertainties that could cause actual results to differ materially from the future results expressed, forecasted, or implied by such forward-looking statements. For a more complete list and description of such risks and uncertainties, refer to Technicolor’s filings with the French Autorité des marchés financiers.

About Technicolor: www.technicolor.com Technicolor shares are admitted to trading on the regulated market of Euronext Paris (TCH) and are tradable in the form of American Depositary Receipts (ADR) in the United States on the OTCQX market (TCLRY).

Investor Relations

Media

Alexandra Fichelson Alexandra.fichelson@technicolor.com