Innovative AndroidTV™, Linux, and RDK-powered video solutions and smart media devices enable you to deliver high-quality video services with a modern, AI-enhanced user experience including live TV, streaming, advanced surround-sound, and beyond.

From high-definition satellite, off-air, and streaming headend solutions to revolutionary 4K UHD video management systems, Vantiva’s multi-client solutions offer everything you need to elevate the customer experience while satisfying content owners.

Today’s consumers have choices. They demand better, faster, more reliable, and affordable services. Earning satisfaction and loyalty means providing the best customer experience possible — and our extensive experience and expertise in the connected home will ensure you do just that.

ECO Service Management is a cloud-based platform that simplifies the delivery of next-generation services and manages the complexities of blending emerging consumer devices and next-generation technology. It supports mission-critical service management that empowers customer support, operations, and subscribers.

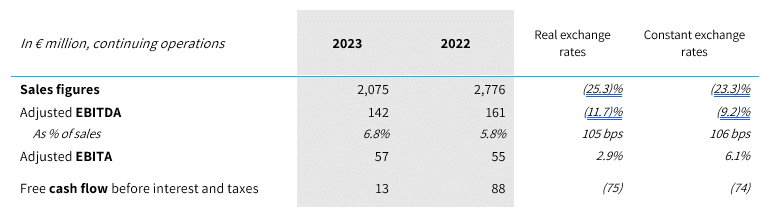

Strong margin resilience in a difficult environment Adjusted EBITDA of 142 million euros Adjusted EBITDA margin up 1 point to 6.8% of sales Adjusted EBITA at 57 million euros Positive FCF (before interest and tax) of 13 million euros The group confirms the potential of synergy resulting from Home Networks acquisition

Paris – March 26, 2024 – Vantiva (Euronext Paris: VANTI), announces its financial results for the year 2023. These results were approved by the Board of Directors today.

The audit procedures on the consolidated financial statements have been completed, and the certification report will be issued once the verification of the management report and the due diligence relating to the electronic ESEF format of the 2023 financial statements have been finalized.

Results for the 2023 financial year are in line with targets, despite the difficult economic climate.

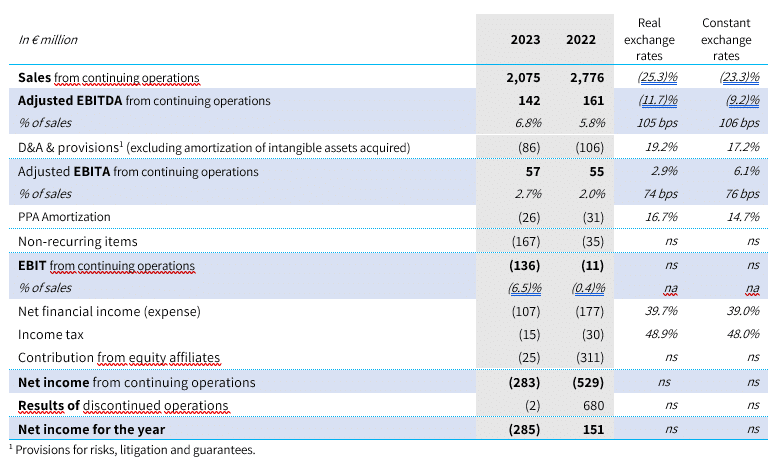

Sales fell by 25.3% to 2,075 million euros (-23.3% at constant exchange rates).

Adjusted EBITDA totaled 142 million euros (-11.7%), with the margin rising to 6.8% of sales from 5.8% in 2022.

Adjusted EBITA rose slightly to 57 million euros (versus 55 million euros in 2022).

Net income from continuing operations was a loss of 283 million euros, compared with a loss of 529 million euros in 2022, which took into account a negative contribution of 311 million euros from equity-accounted earnings resulting from the impairment of the value of TCS shares.

Group net income was a loss of 285 million euros, compared with a profit of 151 million euros, which included a profit of 680 million euros from “discontinued operations”, mainly due to the distribution of TCS shares.

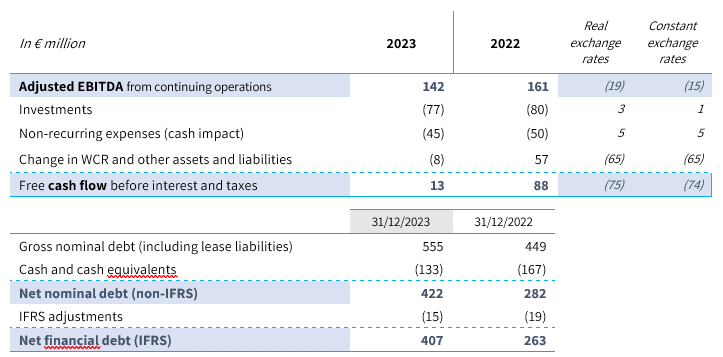

Free cash flow, before interest and taxes, was positive at 13 million euros, down by 75 million euros compared with 2022, due to the decline in EBITDA and above all to the negative impact of changes in working capital.

At year-end, Vantiva held cash and cash equivalents of 133 million euros and an undrawn credit line of 76 million euros.

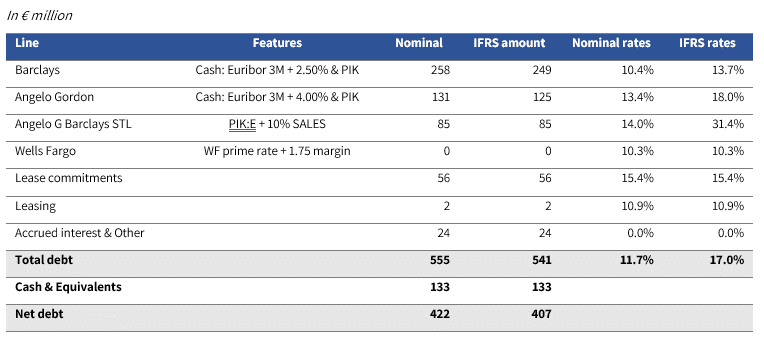

Total net debt (excluding asset leases) amounted to 366 million euros (nominal).

Luis Martinez-Amago, Chief Executive Officer of Vantiva, said:

“We are proud to have achieved our targets against a backdrop of reduced customer orders in both our Connected Home where customers are still holding excess inventories and Supply Chain Solutions where the new diversified offer is still not compensated the natural decline in Disks. The strong resilience shown by our improved adjusted EBITDA margin, despite the significant drop in sales, demonstrates the company’s agility and responsiveness in responding to a highly volatile environment in a context of cost inflation. This performance gives me particular confidence in the successful integration of the acquisition of CommScope’s Home Networks business. This acquisition is a strategic turning point for Vantiva and ideally positions the group to meet the challenges of our industry and achieve unprecedented financial results for the company. I would like to thank all our teams for their commitment, without which these results would not have been possible”.

Key points 2023 and outlook 2024

Key points 2023

The group’s business was penalized by the general economic environment and the reduction in investment budgets by major telecom network and cable operators, against a backdrop of high inventories. The company’s responsiveness to this situation enabled it to limit the decline in adjusted EBITDA in absolute terms, and to improve the margin as a percentage.

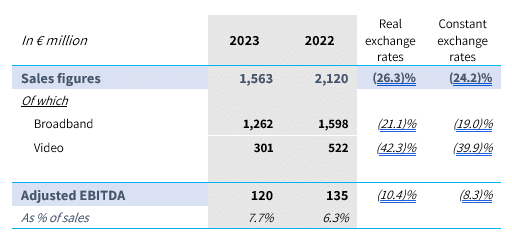

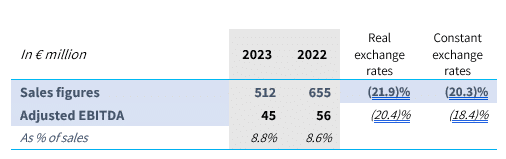

Vantiva sales totaled 2,075 million euros, down 25.3% (-23.3% at constant exchange rates). “Connected Home” contributed 1,563 million, down 26.3% (-24.2% at constant exchange rates), while “Supply Chain Solutions” sales fell by 21.9% to 512 million euros (-20.3% at constant exchange rates).

Adjusted EBITDA came to 142 million euros for the group. The decline in this indicator was limited to 19 million euros. This decline was mainly due to the impact of lower sales in both divisions, largely but not totally offset by cost-cutting measures and tight control of central costs. The contribution of “Connected Home” is 120 million euros (compared with 135 million in 2022) and that of “Supply Chain Solutions” 45 million euros (compared with 56 million in 2022).

Cost-containment measures improved EBITDA margin, which rose by 105 basis points to 6.8% of sales. Free cash flow before financial expenses and taxes is positive at €13 million, compared with €88 million in 2022. This deterioration is largely explained by lower EBITDA and the negative impact of changes in working capital.

Outlook

The beginning of the year confirms that 2024 should be another challenging year for Connected Home business. Major telco operators are cutting their capex program for the year and this will weigh on demand for CPE. We are expecting the market to start to recover by the end of 2024.

For Supply Chain Solutions, Vantiva anticipates a natural decline in demand for optical discs, and an increase in sales for “growth activities”. The increase in vinyl records production capacity should continue to be one of the main growth drivers in this area.

Against this backdrop, Vantiva management will be focused on the success of Home Networks’ integration and will continue to make the needed structural adjustments for preserving the profitability.

For the fiscal year 2024, the group aims to achieve the following:

Adjusted EBITDA > €140 million

FCF(1)> €0 million

(1)After financial expenses and taxes and before restructuring and integration costs related to HN acquisition.

This outlook is based on a €/$ parity assumption of 1.08.

By 2026, the management is confident that Vantiva will generate a sustainable and healthy positive FCF, after interest, tax and restructuring costs.

Analysis by division – Highlights of 2023 results

Connected home

Breakdown of sales by product

The contribution of the Connected Home division accounted for 75% of group sales (versus 76% in 2022) and totaled 1,563 million euros, down 26.3%. At constant exchange rates, the decline would have been -24.2% compared with 2022. This is primarily the result of falling volumes in all regions where the group is active, due to reduced investment programs by telecom and cable network operators. Broadband products, especially fiber, held up better than video products, which were particularly hard hit, notably in North America, by the decline in Android TV products. Broadband accounted for over 80% of the division’s sales, compared with 75% the previous year.

The division’s adjusted EBITDA represented 85% of the group total, versus 84% in 2022. It amounted to 120 million euros for 2023 versus 135 million in 2022, or 7.7% of sales (6.3% in 2022). This increase in the margin rate illustrates the cost-cutting measures rapidly deployed to offset the decline in activity.

Supply Chain Solutions

Sales and EBITDA

Sales for the “Supply Chain Solutions” division amounted to €512 million in 2023, down 21.9% on 2022. At constant exchange rates, the decline would have been -20.3%. The structural decline in optical disc sales was amplified by the downturn in consumer discretionary spending, particularly in North America, but partially offset by price increases. Other logistic activities remained relatively stable despite this unfavorable environment. Vinyl record sales rose following the commissioning of new production capacity. The division’s adjusted EBITDA amounted to 45 million euros (vs. 56 million in 2022), representing 8.8% of sales vs. 8.6% in 2022. The decline was limited thanks to cost reductions, price increases and the ramp-up of the vinyl record business. As a result, adjusted EBITDA margin improved by 17 basis points.

Corporate & Other

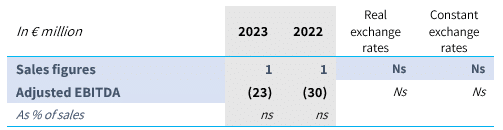

Corporate & Other recorded sales of 1 million euros, as in 2022. Adjusted EBITDA amounted to -23 million, an improvement of 7 million euros in 2022 due to strict control of central services operating expenses.

Income statement analysis

Income statement

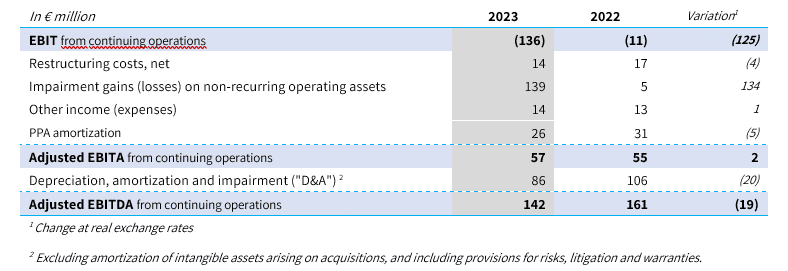

Sales for 2023 amounted to 2,075 million euros, down 25.3% (-23.3% at constant exchange rates), due to the downturn in our main markets for “Connected Home”, notably in North America, and for video decoders. The contribution of the “Supply chain Solutions” division fell by a similar amount, due to the continuing downturn in the DVD business, marginally offset by an increase in growth activities. Adjusted EBITDA totaled 142 million euros, down 11.7% and 9.2% at constant exchange rates. By contrast, adjusted EBITDA margin improved by 105 basis points to 6.8% of sales. This improvement, against a backdrop of a significant contraction in business, reflects the impact of cost-cutting measures which were implemented rapidly and effectively. Adjusted EBITA of €57 million was up €2 million despite the fall in adjusted EBITDA, due to lower depreciation and provisions. PPA amortization totaled -26 million euros, compared with 31 million euros.

Non-recurring items showed a negative balance of 167 million euros, due to:

Restructuring costs of -14 million euros, compared with -17 million in 2022, following a drop in expenses for “Supply Chain Solutions” and Corporate, while they increased by 2 million for “Connected Home”;

Other income and expenses, which represented an expense of -14 million euros versus -13 million euros the previous year, mainly due to costs incurred in connection with the acquisition of Home Networks;

Impairment losses on non-current assets of -139 million euros (vs. -5 million in 2022) following the impairment of “Supply Chain Solutions” goodwill recorded in the first half of the year.

As a result, EBIT is negative by -136 million euros, compared with a loss of -11 million in 2022. Net financial expense amounted to -107 million euros for 2023, compared with -177 million the previous year. Net interest expense on debt (excluding asset leases) came to -70 million euros, compared with -167 million euros in 2022. It should be remembered that the cost of debt in 2022 was impacted by the cost of early repayment of debt prior to completion of the Spin-Off. Other financial expenses of -37 million euros were mainly due to impairment of TCS assets and an increase in pension commitments. Income tax amounted to -15 million euros, compared with -30 million euros in 2022. Equity-accounted income was a loss of -25 million euros versus -311 million euros in 2022, mainly due to the impairment of the value of the 35% stake in TCS. Net income from continuing operations for the year was therefore -283 million euros, compared with -529 million euros in 2022. Group net income was a loss of -285 million euros, compared with a profit of 151 million euros, which took into account the gain on the valuation of TCS at the time of the Spin-Off.

Cash Flow and debt analysis

Free cash flow before interest and taxes fell from +88 million euros to +13 million. This decline was due to adjusted EBITDA (-19 million), and changes in working capital (-65 million), while capital expenditure and restructuring costs were down by 3 and 4 million euros respectively. The change in working capital requirements is mainly due to the negative impact of lower sales and customer order deferrals. Pension commitments fell by 10 million euros after taking into account payments made for 28 million euros, a negative actuarial effect of 7 million euros and a net charge for the year of 12 million euros. Cash out for restructuring amounted to -18 million euros versus -22 million euros. Capital expenditure amounted to -77 million euros, a decrease of 3 million euros compared to 2022. Most of this was R&D capital expenditure. The cash position at the end of December 2023 was 133 million euros, compared with 167 million euros a year earlier. Nominal net debt at the end of the year stood at 422 million euros, an increase of 140 million due mainly to negative FCF (after interest and tax cash out), non-cash interest and new leases. Under IFRS, net debt was €407 million at December 31, 2023.

Post-closing event

On October 3, 2023, the group announced an agreement to acquire CommScope’s home connectivity business. This acquisition was finalized on January 9, 2024. For further details, please refer to the press releases published on these dates and available on our website.

Appendice 1

Debt details

Appendice 2

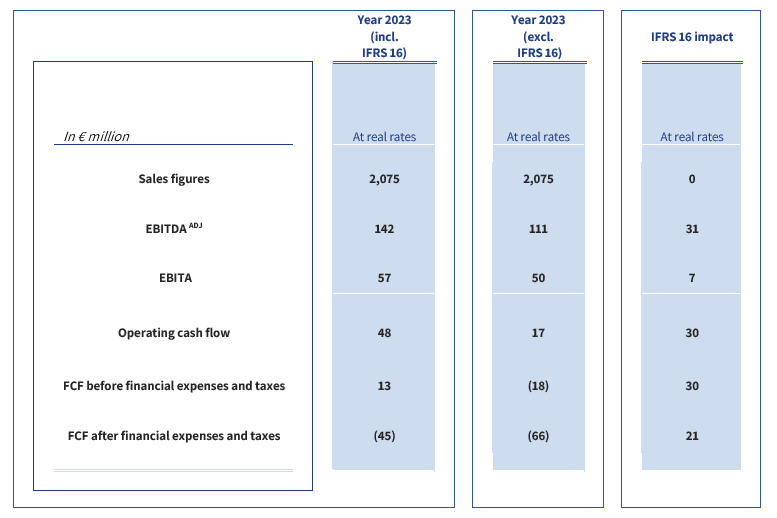

Impact of IFRS 16

Appendice 3

Reconciliation of indicators 4

In addition to the published results, and to enable better comparability of operating performance trends in 2023 versus 2022, Vantiva presents a set of adjusted indicators which exclude the following items as presented in the group’s consolidated income statement and financial statements:

Net restructuring costs;

Expenses net of asset impairment;

Other income and expenses (other non-recurring items).

Adjusted EBITDA corresponds to income from continuing operations before tax and net financial income, excluding other income and expenses, depreciation and amortization (including the impact of provisions for risks, guarantees and litigation). Adjusted EBITA corresponds to income from continuing operations before tax and net financial income, excluding other income and expenses and impairment of PPA items.

###

Warning: Forward Looking Statements This press release contains certain statements that constitute “forward-looking statements”, including but not limited to statements that are predictions of or indicate future events, trends, plans or objectives, based on certain assumptions or which do not directly relate to historical or current facts. Such forward-looking statements are based on management’s current expectations and beliefs and are subject to a number of risks and uncertainties that could cause actual results to differ materially from the future results expressed, forecasted, or implied by such forward-looking statements. For a more complete list and description of such risks and uncertainties, refer to Vantiva’s filings with the French Autorité des marchés financiers (AMF). The Universal Registration Document (Document d’enregistrement universel) for fiscal year 2022 was filed with the Autorité des marchés financiers on April 26, 2023, under no. D.23-0337, and an amendment was filed with the Autorité des marchés financiers on December 8, 2023, under no. D.23-0337-A01.

###

About Vantiva

Pushing the Edge Vantiva shares are admitted to trading on the regulated market of Euronext Paris (VANTI). Vantiva, formerly known as Technicolor, is headquartered in Paris, France. It is an independent company which is a global technology leader in designing, developing and supplying innovative products and solutions that connect consumers around the world to the content and services they love – whether at home, at work or in other smart spaces. Vantiva has also earned a solid reputation for optimizing supply chain performance by leveraging its decades-long expertise in high-precision manufacturing, logistics, fulfillment and distribution. With operations throughout the Americas, Asia Pacific and EMEA, Vantiva is recognized as a strategic partner by leading firms across various vertical industries, including network service providers, software companies and video game creators for over 25 years. The group’s relationships with the film and entertainment industry goes back over 100 years by providing end-to-end solutions for its clients. Following the acquisition of CommScope’s Home Networks in January 2024, Vantiva continues its 130-year legacy as a global leader in the connected home market. Vantiva is committed to the highest standards of corporate social responsibility and sustainability across all aspects of their operations. For more information, please visit vantiva.com and follow Vantiva on LinkedIn and Twitter. Contacts